The Fuel Emissions Trading Act (BEHG), which came into force on 20.12.2020, will apply to the heating and transport sectors from 2021.

The SESTA regulates the pricing of fossil greenhouse gas emissions in the heat and transport sectors and is intended to make a substantial

Greenhouse gas neutrality in Germany 2050

contribute to the

The SESTA covers emissions from heat generation in the buildings sector, from energy and industrial installations outside the EU Emissions Trading Scheme (EU ETS), and emissions from the combustion of fossil fuels. Air transport, which is subject to the EU ETS, is not affected by SESTA.

Even though 14 regulations are still missing in February 2020, which largely regulate the requirements of the affected companies, GALLEHR+PARTNER® can already make a statement on the groups of companies that are fundamentally affected:

Who is affected by SESTA?

The effects of the BEHG will probably be felt indirectly by the entire German population, since the CO2 price is expected to lead to higher fuel costs in general.

Direct costs and administrative overheads arise for the following companies:

1. distributors of fuels:

Distributors

of fuels are around 4000 companies that market fuels according to Annex 1 of the SESTA. In 2021 and 2022, these fuels are limited to petrol, gas oils, heating oils, natural gas and liquefied gases (see Annex 2).These companies must submit a (simplified) monitoring plan and emissions report to the Federal Environment Agency (presumably DEHSt) and surrender a certificate per tonne of CO2 on the basis of the annually determined emissions.

In the explanatory notes to the first draft of the law dated 05.11.2019, the distributors were specified as follows:

„In the process, in accordance with the The system of energy tax law obliges companies to participate at the level of trade at which, in the case of the Energy Tax Act for the placing on the market of energy products the tax – irrespective of tax exemptions – arises in principle. In the case of mineral oil products, for example, these are predominantly the distributors (first stage of trade), whereas in the case of natural gas they are the suppliers (last stage of trade).”

2. undertakings subject to the EU ETS:

Companiessubject to EU emissions trading under the TEHG are to be protected from a so-called “

Double burden

” by the SESTA. According to Section 7 (5) SESTA, the double burden is to beavoided as far as possible in advance, especially in the case of direct deliveries. The exact procedures and requirements are to be clarified in the course of 2020 in a legal ordinance.

From the point of view of GALLEHR+PARTNER® it can be assumed that almost every operator of a plant subject to emissions trading will be confronted with new administrative requirements. Without the cooperation of these companies, it will, for example. it will be difficult for distributors to draw a clear line between the two.

The legislator already anticipates this aspect to the extent that it intends to regulate in a separate statutory instrument how installation operators who are nevertheless exposed to a double burden can receive full financial compensation.

3. undertakings with very high fuel costs – Undue hardship

Companies for which the additional costs incurred as a result of SESTA account for more than 20% of gross value added or 20% of total business costs are to be given the opportunity to apply for financial compensation(cf. §11 para. 1). The extent to which this will be done and whether the percentage of 20% will be maintained are to be regulated in a subsequent legal ordinance.

4. companies that manufacture products at risk of relocation (carbon leakage)

Protection is envisaged for companies facing strong international competition. A further legal ordinance is to regulate the avoidance of

Carbon leakage

(leakage of C02 emissions out of Germany) from 2022 onwards. Competitiveness is to be achieved through earmarked financial support for climate-friendly investments.

GALLEHR+PARTNER® assumes that companies wishing to receive appropriate financial support must, for example, carry out the following verification requirements:

- Evidence of the risk of displacement by means of NACE or PRODCOM codes.

- Evidence of planned measures in climate-friendly investments

- Proof of the costs of the climate-friendly investments carried out

- Evidence of methods for monitoring the effectiveness of investments, such as the implementation of

standard-compliant energy audits

or the existence of

Energy management systems according to ISO 50001

GALLEHR+PARTNER® supports affected companies on all issues relating to the Fuel Emissions Trading Act (SESTA) and the national Emissions Trading Scheme (nEHS).

We carry out the following activities:

- Determining the impact of the Fuel Emissions Trading Act (SESTA) on your company

- Preparation and submission of the monitoring plan in accordance with §6 BEHG and support up to approval

- Verifiable determination of fuel emissions and preparation of the emissions report pursuant to § 7 para. 1, 2 SESTA

- Preparation and support of the verification of the emission report according to § 7 para. 3 SESTA

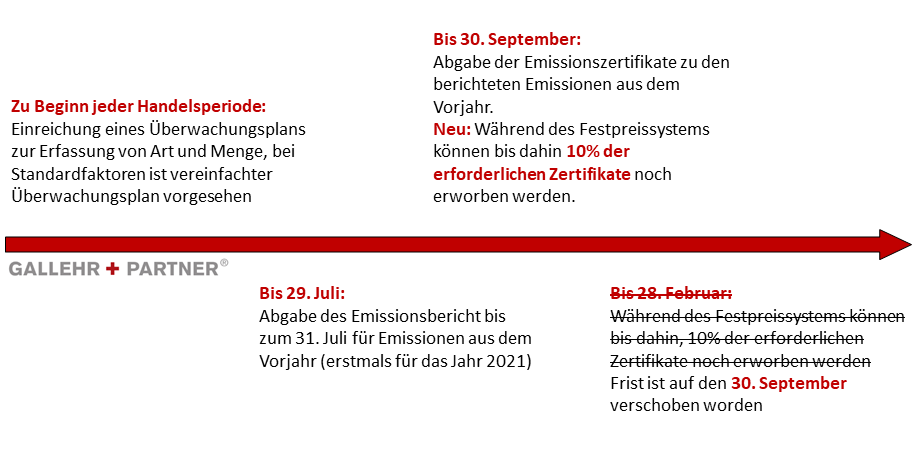

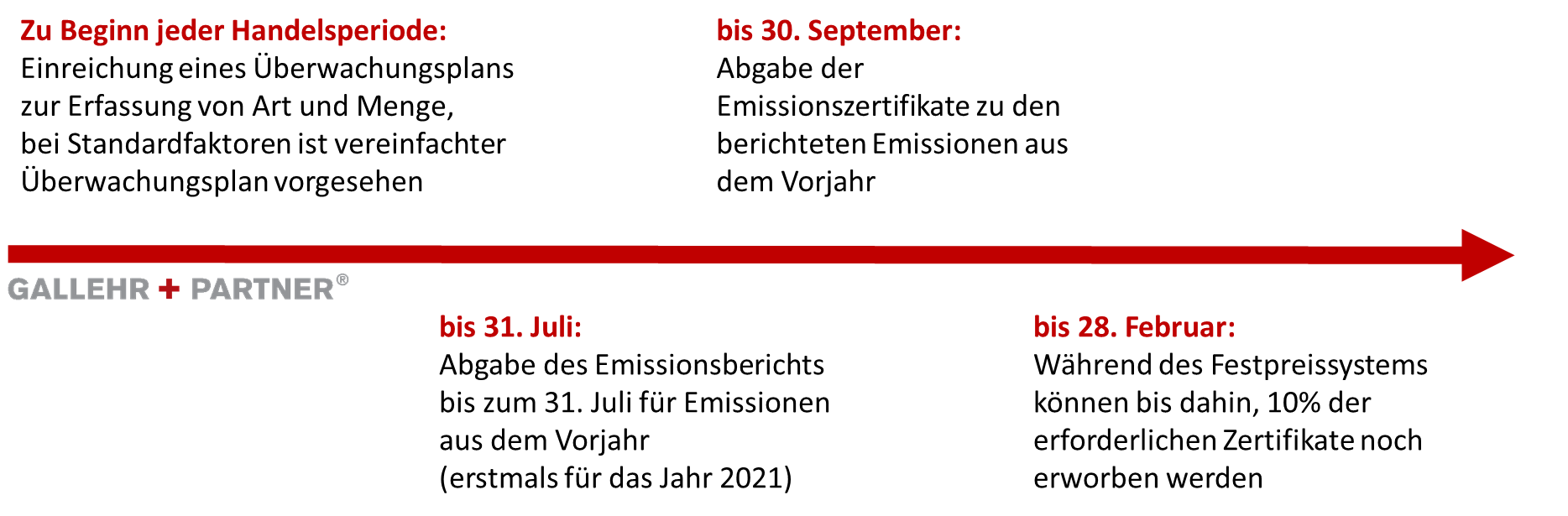

- Transmission of the verified emissions report to the competent authority (DEHSt) by 31.07 of the following year in accordance with §7 Para. 1 SESTA

- Verification of the avoidance of double charging in accordance with §7 Para. 5 SESTA

- Support in the establishment of accounts and account representatives in the national emissions trading registry pursuant to section 12 para. 2 SESTA for the administration of emission allowances pursuant to section 9 para. 1

- Support in the management of their register account e.g. as one of the authorized account holders

- Verification of transfers

- timely retransfers of emission allowances by 30.09 for the previous year pursuant to § 8 SESTA

- Data updates of information in the register

- Representation of historical account movements and balances on the basis of account statements

- Support in the purchase and sale of emission certificates

- Support with requests for information and assistance with on-site inspections by the competent authority pursuant to § 14 SESTA

- Identification of emission allowance price drivers and market monitoring

- Ad hoc announcements on relevant events, political developments and legislative changes

- Regular status and strategy meetings to strengthen decision-making capacity

Secure your non-binding appointment to get to know us now

Author: Marcus Hipp, GALLEHR+PARTNER®

This might also interest you

- The European Emissions Trading Scheme (EU-ETS) and the consequences for affected companies

- Energy management in industry: ISO 50001 as a management system to avoid energy and CO2 costs

The “Fuel Emissions Trading Act” (BEHG), which came into force on 20.12.2020, applies from 2021 to the heating and transport sectors

The BEHG regulates the pricing of fossil greenhouse gas emissions in the heating and transport sectors and is intended to make a significant contribution to Germany’s greenhouse gas neutrality in 2050.

The BEHG covers emissions from heat generation in the building sector, energy and industrial plants outside the EU Emissions Trading Scheme (EU ETS), and emissions from the combustion of fossil fuels. Aviation, which is subject to the EU ETS, is not affected by the SESTA.

Who does the SESTA concern?

The effects of the BEHG will probably indirectly affect the entire German population, since the CO2 price is generally expected to result in higher fuel costs.

Even if there are still 14 ordinances missing in February 2020 that largely regulate the requirements of the companies concerned, GALLEHR+PARTNER® can already make a statement about the groups of companies fundamentally affected:

Direct costs and additional administrative expenses will arise for the following companies:

1. distributors of fuels:

Approximately 4000 companies are placing fuels according to Annex 1 of the SESTA on the market. In 2021 and 2022 these fuels

are limited to petrol, gas oils, heating oils, natural gas and liquefied gases (see Annex 2)

These companies must submit a (simplified) monitoring plan and emissions report to the Federal Environment Agency (probably DEHSt) and issue a certificate per tonne of CO2 on the basis of the annually determined emissions.

In the explanatory notes to the first draft of the law of 05.11.2019, the marketers were specified as follows:

“In accordance with the system of the energy tax law, the companies are obliged to participate at the trade level at which the tax – without prejudice to tax exemptions – is basically incurred in the energy tax law for the marketing of energy products. In the case of mineral oil products, for example, these are mainly the distributors (first level of trade), whereas in the case of natural gas it is the suppliers (last level of trade).”

2 Participants in European emissions trading

Companies subject to EU emissions trading under TEHG are to be protected against a so-called“double burden” from the BEHG. According to paragraph 7(5) SESTA, the double burden should be avoided as far as possible in advance, especially in the case of direct deliveries. The exact procedures and requirements are to be clarified in a statutory instrument in the course of 2020.

From the point of view of GALLEHR+PARTNER® it can be assumed that almost every operator of a plant subject to emissions trading will be confronted with new administrative requirements. Without the involvement of these companies, it will, for example, hardly be possible for the marketers to make a clear distinction.

The legislator anticipates this aspect to the extent that it intends to regulate in a separate statutory instrument how plant operators who are nevertheless exposed to a double burden can receive full financial compensation.

3. companies with very high fuel costs – unreasonable hardship

Companies for which the additional costs incurred as a result of SESTA account for more than 20% of gross value added or 20% of total business costs should be given the opportunity to apply for financial compensation(paragraph 11 (1)). The extent to which this will be done and whether the 20% percentage will be maintained will be regulated in a subsequent ordinance.

4. companies that manufacture products at risk of relocation (carbon leakage)

Protection is planned for companies that are in strong international competition. A further legal regulation is to regulate the avoidance of

carbon leakage

(migration of C02 emissions out of Germany) from 2022 onwards. Competitiveness is to be achieved through earmarked financial support for climate-friendly investments.

GALLEHR+PARTNER® assumes that companies wishing to receive such financial support must, for example, provide the following proof:

- Proof of the risk of relocation using NACE or PRODCOM codes

- Proof of planned measures in climate-friendly investments

- Cost proof of the climate-friendly investments made

- Proof of methods for monitoring the effectiveness of investments, such as conducting

energy audits

in accordance with standards or the existence of

energy management systems in accordance with ISO 50001

GALLEHR+PARTNER® supports affected companies on all issues relating to the Fuel Emission Trading Act (BEHG) and the national emissions trading system (nEHS).

We offer the following activities:

- Preparation and transmission of the monitoring plan according to §6 BEHG and support until approval

- Verifiable determination of fuel emissions and preparation of the emissions report pursuant to Article 7 para. 1, 2 SESTA

- Preparation and support of the verification of the emissions report according to § 7 para. 3 SESTA

- Transmission of the verified emissions report to the competent authority (DEHSt) by 31.07 of the following year in accordance with §7 para. 1 SESTA

- Evidence to avoid double burdens in accordance with §7 para. 5 SESTA

- Support in setting up accounts and authorised representatives in the national emissions trading registry pursuant to § 12 para. 2 SESTA for the administration of emissions allowances pursuant to § 9 para. 1

- Support in the administration of your registry account, e.g. as one of the authorised representatives

- Checking account transfers

- Timely retransfer of emission certificates by 30.09 for the previous year in accordance with § 8 BEHG

- Data updates of information in the register

- Presentation of historical account movements and balances on the basis of account statements

- Support for the purchase and sale of emission certificates

- Assistance with requests for information and support during on-site inspections by the competent authority in accordance with § 14 BEHG

- Identification of the price drivers of emission allowances and market observations

- Ad hoc – Notifications of relevant events, political developments and changes in legislation

- Regular status and strategy meetings to strengthen the decision-making capacity

Author: Marcus Hipp, GALLEHR+PARTNER®