The border adjustment mechanism forCO2 (CBAM)

Way clear for CBAM

On March 15, 2022, the Economic and Financial Affairs Council (ECOFIN Council) adopted by a large majority the draft regulation of theCarbon Border Adjustment Mechanism (CBAM), which is considered a new key element of the “fit for 55 package” in the context of the European Emissions Trading System. With the approval of the finance ministers, the EU will have another climate policy system available in the near future (2026) to achieve climate targets (the Green Deal), which will operate in parallel with the European Emissions Trading Scheme (EU ETS). The European Parliament, which is involved in the decision-making process, will vote on the project in plenary session in June 2022.

What is CBAM?

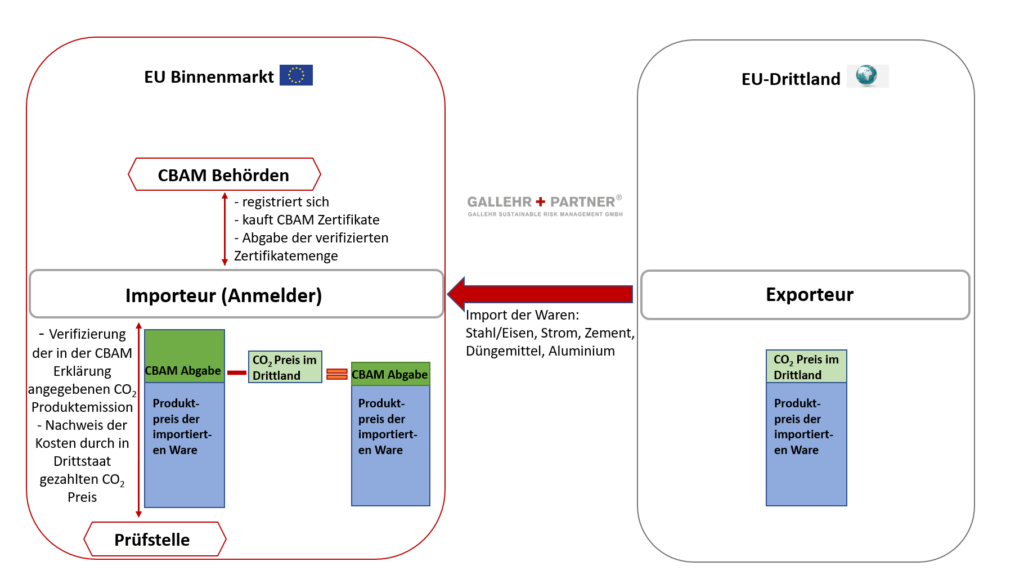

With the help of theCO2 border adjustment mechanism CBAM, levies are to be imposed throughout the EU from 2026 on various goods whose production in non-EU countries causesCO2 emissions. The aim of the system is to compensate for cost disadvantages of companies that are subject toCO2 pricing in the EU and have to compete with less stringent climate protection requirements compared to producers in other EU countries. This is intended to counteract the “carbon leakage” problem: the distortion of competition in the import ofCO2-intensive products and the resulting relocation of production to third countries with no or lowerCO2 pricing.

Who is affected?

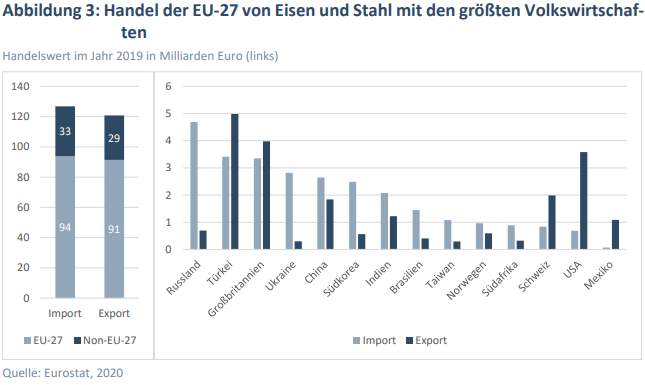

For the time being, only importers in the EU who purchase the following basic material groups (see pp.76-86) (products) from other EU countries are directly affected by the CBAM: Cement, iron, steel, aluminum, fertilizer and electricity.

By the end of the transition period, the EU Commission will evaluate the CBAM success and decide whether the scope will be extended to other products and services (also along the value chain).

What impact will the CABM have on the free allocation of EU-ETS allowances?

CBAM is expected to have a far-reaching impact on the free allocation of EU-ETS allowances. The border adjustment system is intended to completely replace the free allocation of EU-ETS allowances as a mechanism for avoiding “carbon leakage” from 2035. The free allocation for the affected sectors is likely to be reduced significantly more than previously planned with the introduction of CBAM from 2026. Accordingly, there is a close connection with the EU ETS. However, there is still no final agreement on the reduction of free allocation in European emissions trading, as this would have to be clarified as part of a reform of the European emissions trading system.

Smaller manufacturers of the affected products in the EU who are not regulated in the EU ETS may even have a (temporary) competitive advantage in the future as a result of CBAM.

What’s in store for those affected?

Importers affected by CBAM must register with the national authorities from which they also purchase CBAM certificates. They approve the registration, check and verify the declarations of the applicants. However, greater centralization of the system is envisaged, including the creation of a new register for importers at EU level.

Supplies below 150 euros are not affected by the mechanism, as they are below the minimum threshold decided.

When does the regulation come into force?

In a transitional phase, from January 1, 2023 until the end of 2025, importers will be subject to a reporting obligation for the above-mentioned (CO2-intensive ) basic materials without having to pay a financial levy.

Starting in 2026, the “arming” of the mechanism will result in a levy on direct emissions (released directly during the manufacturing process) of imported goods covered by the CBAM.

What information must be included in the CBAM report?

According to the CBAM Regulation of March 15, 2022, each importer shall submit to the Commission for each quarter, not later than one month after the end of the quarter, a report on the goods imported during the previous quarter with the following information:

- Total quantity of each type of commodity in megawatt-hours for electricity and in tons for other commodities, broken down by the facilities producing the commodities in the country of origin;

- Actual total gray (direct, manufacturing) emissions in metric tons ofCO2 emissions per megawatt-hour of electricity or, for other commodities, metric tons ofCO2 emissions per metric ton of each commodity type;

- total indirect emissions in the unit in accordance with the procedure described in an implementing act;

- CO2 price that must be paid in a country of origin for the gray emissions associated with the imported goods.

The gray emissions of imported goods are determined on the basis of direct emissions in accordance with specified procedures. They must be communicated to EU importers by manufacturers outside the EU. Since it is difficult or costly to record the exactCO2 emissions of many imported goods, the emissions are determined on the basis of standard values (benchmarks) if there is a lack of information (from the manufacturer). The measurability of the actualCO2 impact varies greatly from industry to industry.

Who collects CBAM levy and verifiesCO2 data?

Verification of these default values and the established procedures is the responsibility of the national competent authority. From GALLEHR+PARTNER®’s point of view, it seems obvious that either the German Emissions Trading Authority (DEHSt) or the main customs office in Germany will be responsible.

In a border adjustment declaration, EU importers affected by the CBAM must report the volume of goods imported into the EU in the previous year and the emissions contained therein by May 31 of each year, starting in 2026.

What information must the CBAM statement contain and where must it be filed?

- The total quantity of each type of commodity imported in the preceding calendar year in megawatt-hours for electricity and in tons for other commodities;

- total gray emissions of these goods in metric tons ofCO2 emissions per megawatt-hour of electricity or, for other goods, in metric tons ofCO2 emissions per metric ton of each type of goods;

- the total number of CBAM allowances corresponding to total gray emissions that must be surrendered, after mitigation based on theCO2 price paid in a country of origin and after the required adjustment corresponding to the extent to which EU ETS allowances are allocated for free.

- It must be submitted to the Central Registry (yet to be established).

CBAM Regulation 15 March 2022 p.38

The competent authority of the Member State may review a CBAM declaration within the period ending with the fourth year after the year in which the declaration should have been submitted. Verification may consist of checking the information contained in the CBAM declaration on the basis of the information provided by the customs authorities and other relevant evidence.

The importer simultaneously surrenders the number of CBAM certificates corresponding to the emission volume of its products.

(https://ec.europa.eu/commission/presscorner/api/files/attachment/869376/CBAM_factsheet.pdf.pdf)

Indirect emissions (emissions generated during mining, processing of feedstocks, and electricity, heat, or gas generation required for the production process) are not included/calculated in the current CBAM regulation, but are under discussion/review for future revisions of the CBAM.

However, according to the EU Commission’s FAQ, importers have the option to prove actual emissions in a reconciliation process and surrender the appropriate number of CBAM allowances.

How much will the CBAM levy be?

According to the Commission proposal approved by the ECOFIN Council, the amount of the CBAM levy would be determined by theCO2 intensity of the product concerned and the average EU ETS price. Thus, the price of the CBAM levies is based on the EU-ETS market, but unlike the latter, it does not have a cap (upper limit of allowances). It is thus effectively a fictitious ETS in which imports do not compete with domestic production for the same limited quantity of allowances.

There is also the question of whether, in the course of the CBAM regulation, EU exporters will be relieved of higherCO2 levies compared to EU third countries, in order to counter their competitive disadvantages in exports to a greater extent. This would be in line with the consistent implementation of the destination principle:CO2 pricing in the respective country of consumption. However, according to the ECOFIN Council, the European Commission is to assess the impact of the CBAM on exports to third countries only in 2026 so far.

Is there any relief planned for smaller companies?

It is to be examined which (specific) exemption and support regulations can be integrated specifically for small and medium-sized enterprises to reduce the administrative burden (as a result of the complex implementation of the CBAM).

What can companies do to reduce the burden?

Importers Directly Affected:

For importers, the Scope 1 greenhouse gas intensity(includes the direct release of climate-damaging gases in their own company) will become an important selection criterion after the introduction of CBAM. Total import costs become lower the less Scope 1 GHG emissions the product being imported has caused during production.

The possibility of smaller order quantities in order not to exceed the minimum threshold of 150 euros is likely to be an unrealistic option in most companies (supply contracts, quantity discounts, fraud).

Companies regulated under EU-ETS:

The instrument for action is the decarbonization of the company’s own production (emission reduction of the production process).

Can I pass on my additional costs as a producer?

According to the Institut der Deutschen Wirtschaft, the ability to pass onCO2 costs depends on the respective market constellation. For example, passing onCO2 costs is far less likely for standardized products such as long steel and structural steels (many suppliers) in international competition than for high-quality steel products (few suppliers).

In the future, CBAM will no longer allow European commodity demanders to rely on suppliers from third countries withoutCO2 costs, which will reduce their market power as demanders. European basic material producers, who are included in the EU ETS and consequently have to bearCO2 costs, are strengthened in their market power by CBAM and the reduction of the free allowance allocation, since there are hardly any competitors withoutCO2 costs when selling in the EU. It should therefore be possible to pass on most of the additional costs. However, the situation is different for exports to third countries. Here, European producers continue to face competition from companies with low or noCO2 costs.

Winners and losers

European companies producing domestically in the EU with a low share of imported feedstock and at the same time having to bear EU ETS-related costs could benefit (CBAM-related) from rising domestic and export prices and increase their market shares compared to other competitors more affected by CBAM.

However, due to its high dependency on imported basic materials, the German export industry could experience an additional cost burden as a result of the CBAM and suffer competitive disadvantages in important export markets with a low C02 price level (e.g. India, China), unless it is brought into line with theCO2 price level of the target country.

Since the planned abolition of free allocation of emission rights is unlikely to be sufficient as an incentive for investments in low-emission technologies in terms of competitiveness, support instruments and measures for (leapfrog) innovations (e.g. the CCfD) provided for in the legal framework of carbon leakage protection are under discussion. They are to be funded from CBAM revenues.