Consultation on the adaptation of the electricity price compensation guidelines for the 4th trading period of the EU greenhouse gas emissions trading scheme is underway.

In the context of the European Greenhouse Gas Emissions Trading Scheme (EU ETS), the EU Commission has published the revised draft guidelines on electricity price compensation for the 4th trading period. Citizens and stakeholders have the opportunity to comment on the Commission’s proposal until 10.03.2020.

The main points of the draft guidelines are set out below. The full draft guidance can be found here.

What is at issue?

Aid measures to compensate for indirect CO2 costs, also known as “electricity price compensation“, are intended to prevent the “risk ofcarbon leakage” and to create incentives for modernisation measures in production processes. In particular, so-called carbon leakage endangered economic sectors, i.e. those economic sectors in the EU that are not covered by the European

CO2 emissions trading system are burdened in such a way that their competitiveness is called into question, should be protected and remain internationally competitive.

What changes compared to the third trading period?

No more mention of investment aid schemes for high-efficiency power plants.

Where the existing Guidelines still address the issue of investment aid for high-efficiency power plants, this area is missing in the new draft Guidelines:

|

3 HP (Valid until 2021) |

4 HP (draft from 2021) |

|

‘‘Aid to compensate for the increase in electricity prices resulting from the inclusion of greenhouse gas emission costs from the EU ETS (aid for indirect CO2 costs)”. |

‘‘Aid to compensate for the increase in electricity prices resulting from the inclusion of greenhouse gas emission costs from the EU ETS (aid for indirect CO2 costs)”. |

|

”Investment aid for high-efficiency power plants, including new power plants suitable for the capture and storage of CO |

Not mentioned |

Cumulation possible in the future

The new draft guidelines describe in paragraph 32 the possibility of cumulation.

“32. The aid may be cumulated with:

- a.) other State aid for other identifiable eligible costs,

- (b.) other State aid in respect of the same eligible costs which overlaps, in part or in whole, and other State aid in respect of which there are no identifiable eligible costs, provided that such cumulation does not result in the maximum aid intensity or aid amount for such aid being exceeded under this section.”

On the one hand, aid for indirect CO2 costs should be able to be cumulated with other State aid for other eligible costs and, on the other hand, with aid for the same eligible costs. This has not been possible up to now.

Fewer sectors are eligible for aid

The current 15 eligible sectors are to be reduced to only 8. The sectors are selected on the basis of the criteria described in Article 10b of the revised ETS Directive, which are also defined for the ETS Carbon Leakage List.

It follows that only the following sectors will be eligible for aid:

| NACE code | Description | |

| 1. | 14.11 | Manufacture of leather garments |

| 2. | 24.42 | Production and initial processing of aluminium |

| 3. | 20.13 | Production of other inorganic basic materials and chemicals |

| 4. | 24.43 | Production and first processing of lead, zinc and tin |

| 5. | 17.11 | Production of wood and pulp |

| 6. | 17.12 | Production of paper, cardboard and paperboard |

| 7. | 24.10 | Production of pig iron, steel and ferroalloys |

| 8. | 19.20 | Mineral oil processing |

In future, however, it will be possible to include further sectors if criteria under Article 10b of the revised ETS Directive are met and a medium carbon leakage risk is identified.

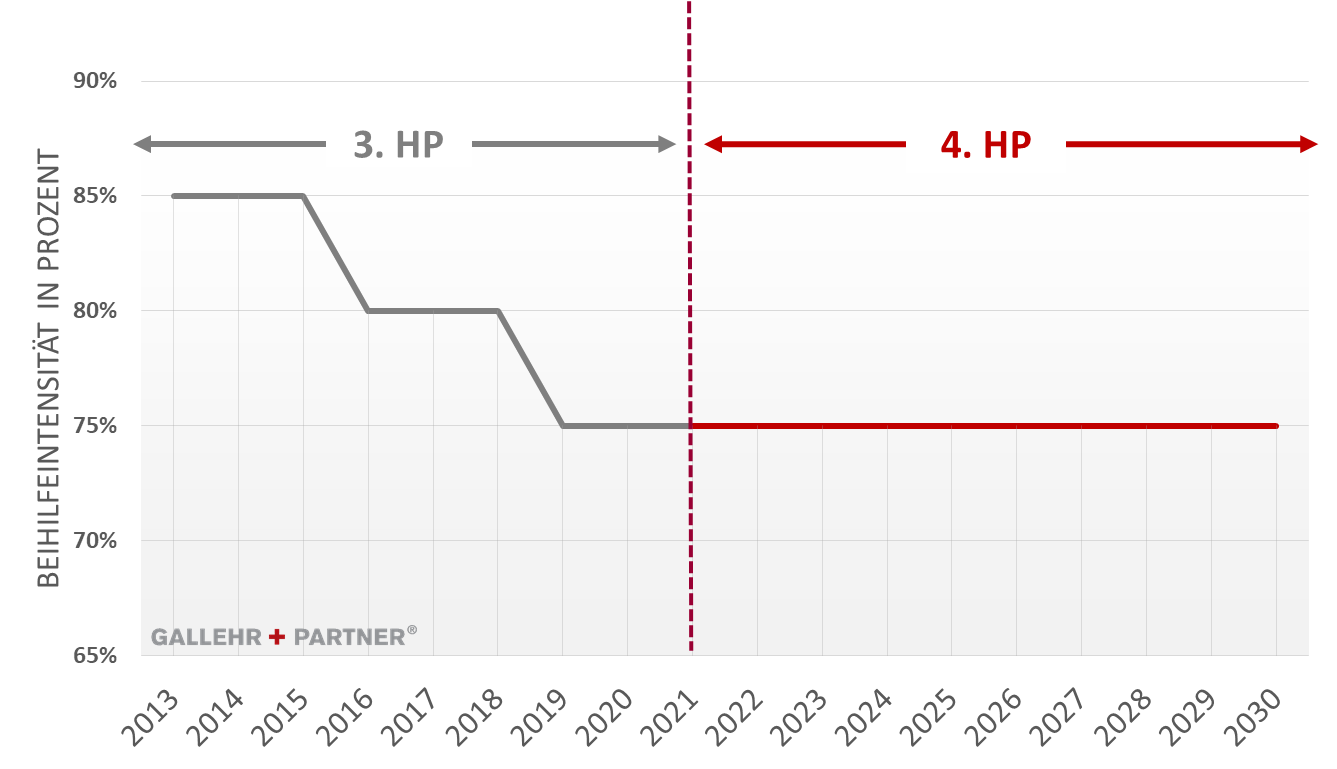

Unchanged aid intensity

As at the end of the 3rd trading period, the aid intensity is to be a maximum of 75 percent of the indirect CO2 costs incurred. A reduction of this value in the course of the 4th trading period is not foreseen. Instead, the electricity consumption efficiency benchmark is to be adjusted at the beginning (2021) and in the middle (2026) of the 4th emissions trading period. In the opinion of the EU Commission, this would be a better way of taking account of efficiency gains in the relevant sectors.

Possibility of reducing the own contribution

In future, individual Member States should be able to further relieve individual aid recipients who bear a disproportionate share of indirect ETS costs by reducing their own contribution.

“Since an aid intensity of 75 % may be insufficient for some sectors to ensure adequate protection against carbon leakage, Member States may, if necessary, limit the amount of indirect costs payable at undertaking level to […] % of the gross value added of the undertaking concerned in year t.” (See Guidelines on certain State aid measures in connection with the scheme for greenhouse gas emission allowance trading after 2021 (paragraph 30).

The percentage share of indirect costs in gross value added required for this relief has not yet been described. The explanatory paper on the draft guidance explicitly asks for comments on this proposal.

New conditions imposed on aid recipients

In future, aid will be subject to conditions relating to the identification and implementation of energy efficiency measures. For example, the implementation of energy audits and the introduction of energy management and environmental management systems.

In addition to implementation, Member States should monitor that:

- “either the recommendations of the energy audit are implemented(precondition: payback period less than 5 years and “proportionate” investment costs)

- or the CO2 footprint of electricity consumption is demonstrably reduced. As an example, the installation of decentralized renewable energy systems to cover at least 50% of the own electricity consumption or the purchase of CO2-free energy is given.

- or at least 80 percent of the amount of the aid is invested in projects that result in significant reductions in the facility’s GHG emissions.”

The following information fits this report:

- Electricity price compensation

- Consulting energy management

- Energy audit

- Emissions trading

- Carbon Footprint

Secure your non-binding appointment to get to know us now

Consultation on the adaptation of the state aid guidelines on electricity price compensation in the 4th trading period of the EU greenhouse gas emissions trading scheme is ongoing

In the framework of the European Greenhouse Gas Emissions Trading Scheme (EU-ETS), the EU Commission has published the revised draft guidelines for electricity price compensation for the 4th trading period. Citizens and stakeholders have the opportunity to comment on the Commission proposal until 10.03.2020.

The most important points of the draft guidelines are set out below. The complete draft guidelines can be found here.

What’s it about?

Aid measures to compensate for indirect CO2 costs, also known as“electricity price compensation“, are intended to prevent the “risk of carbon leakage” and provide incentives for modernisation measures of production processes. In particular, so-called carbon leakage, i.e. those economic sectors in the EU which are so burdened by the EuropeanCO2emissions trading system that their competitiveness is called into question, are to be protected and remain internationally competitive.

What changes compared to the third trading period?

No schemes for investment aid for high-efficiency power plants mentioned any more.

If the existing guidelines still deal with the issue of investment aid for high-efficiency power plants, this area is missing from the new draft guidelines:

|

3 HP (Valid until 2021) |

4 HP (draft from 2021) |

|

Guidelines on certain State aid measures in the context of the system for greenhouse gas emission allowance trading post 2021”. |

Guidelines on certain State aid measures in the context of the system for greenhouse gas emission allowance trading post 2021”. |

|

Investment aid for high-efficiency power plants, including new ones, for the capture and storage of CO |

not mentioned |

Cumulation possible in the future

Paragraph 32 of the new draft guidelines describes the possibility of cumulation.

“32. The aid may be cumulated with:

- a.) any other State aidin relation to different identifiable eligible costs,

- b.) any other State aid, in relation to the same eligible costs, partly or fully overlapping, and any other State aid without identifiable eligible costs,only if such cumulation does not result in exceeding the maximum aid intensity or aid amount applicable to this aid under this section.”

Firstly, aid for indirect CO2 costs should be cumulative with other State aid for other eligible costs and, secondly, aid for the same eligible costs. This is not possible at present.

Fewer sectors are eligible for aid

The current 15 eligible sectors are to be reduced to only 8. The sectors are selected on the basis of the criteria described in Article 10b of the revised EHS Directive, which are also defined for the EHS Carbon Leakage List.

It follows that only the following sectors will be eligible for aid:

| NACE code | description | |

| 1. | 14.11 | Manufacture of leather clothing |

| 2. | 24.42 | Production and first processing of aluminium |

| 3. | 20.13 | Production of other inorganic basic materials and chemicals |

| 4. | 24.43 | Production and first processing of lead, zinc and tin |

| 5. | 17.11 | Manufacture of wood and cellulose |

| 6. | 17.12 | Manufacture of paper, cardboard and paperboard |

| 7. | 24.10 | Production of pig iron, steel and ferroalloys |

| 8. | 19.20 | Mineral oil processing |

However, in the future it should be possible to include further sectors if criteria according to Article 10b of the revised ETS Directive are fulfilled and a medium carbon leakage risk is determined.

Consistent aid intensity

As at the end of the third trading period, the aid intensity should be maximum 75 percent of the indirect CO2 costs incurred. A reduction of this value during the 4th trading period is not planned. Instead, at the beginning (2021) and in the middle (2026) of the 4th emissions trading period, the electricity consumption efficiency benchmark is to be adjusted. In the opinion of the EU Commission, this would be a better way of taking efficiency gains in the relevant sectors into account.

Possibility to reduce the own contribution

Individual Member States should be able to further reduce the burden on individual aid recipients who have to bear a disproportionately high share of indirect ETS costs by reducing their own contribution.

“Given that for some sectors the aid intensity of 75% might not be sufficient to ensure that there is adequate protection against the risk of carbon leakage, when needed, Member States maylimit the amount of the indirect costs to be paid at undertaking level to […] % of the gross value added of the undertaking concernedinyear t.”. (see Guidelines on certain State aid measures in the context of the system for greenhouse gas emission allowance trading post 2021(30)

The percentage of indirect costs of the gross value added necessary for this relief has not yet been described. The explanatory document to the draft guidelines explicitly asks for comments on this proposal.

New conditions imposed on aid recipients

In future, aid will be linked to conditions for the identification and implementation of energy efficiency measures. For example, the implementation of energy audits and the introduction of energy management and environmental management systems should be mentioned.

In addition to implementation, Member States should also monitor that:

- either the recommendations of the energy audit are implemented (prerequisite: payback period of less than 5 years and “proportional” investment costs)

- or the CO2 footprint of electricity consumption is demonstrably reduced. As an example, the installation of decentralized renewable energy systems to cover at least 50% of the own electricity consumption or the purchase of CO2-free energy is given.

- or at least 80 % of the aid amount shall be invested in projects leading to significant reductions of GHG emissions from the installation.

The following information fits this report:

- Electricity price compensation

- Consulting Energy Management

- Energy audit

- Emissions trading

- Carbon Footprint