Innovations – Deadlines – Carbon Leakage Regulations

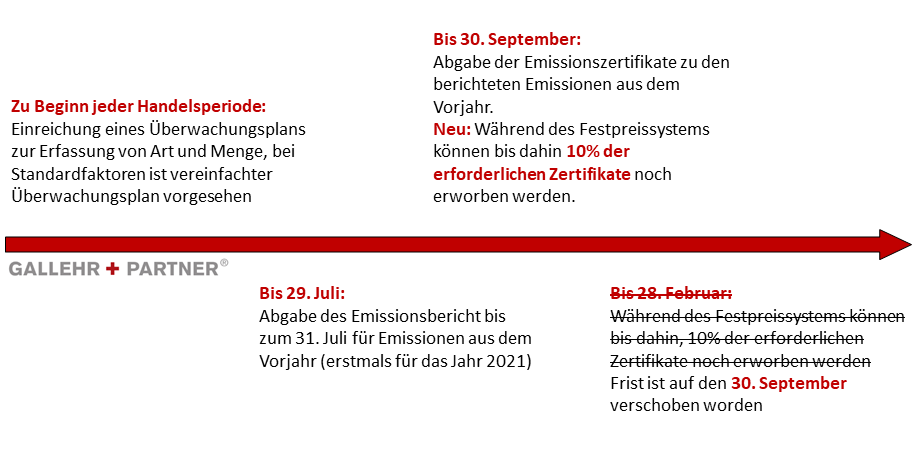

There are again changes to be made to the Fuel Emissions Trading Act (SESTA). On 08/10/2020, the federal government moved the 10% buy-in deadline from Feb. 28 to Sept. 30. This means that the deadline for the purchase coincides with the deadline for the surrender of emission allowances.

Accordingly, the current deadlines have been defined to date as follows:

Pursuant to § 7 paragraph 1 of the SESTA, fuel emission reporting must be recorded by 31 July of the following year.

For the years 2021 and 2022, fuel emissions are to be based on standard emission factors only. From 2022 onwards, a specific monitoring plan will have to be submitted and verified by the competent authority, on the basis of which the respective fuel emissions will be determined.

Furthermore, pursuant to § 8 of the SESTA, the responsible party must surrender by 30 September a number of emission allowances corresponding to the total quantity of fuel emissions reported pursuant to § 7 in the preceding calendar year. This period coincides with the 10% additional purchase period.

Carbon Leakage Regulation to be adopted before the end of 2020

In addition to the deadline changes, there is also movement on the Carbon Leakage (CL) regime. The corresponding regulation is to be adopted in 2020.

On the basis of the published key issues paper, the German government would like to design the compensation regulation for the BEHG on the basis of EU emissions trading. The assessment of relocation risks is also to be carried out by means of a list of sectors. This is intended to take account of the special features of national emissions trading and may accordingly deviate from the European emissions trading sector list.

Note: The respective CL status is based on CO2 intensity and foreign trade intensity. The so-called carbon leakage indicator is defined as the product of the multiplication of the intensity of the sector’s trade with third countries and the emission intensity (in kg) of the sector. If this is above 0.2, there is a risk of CO2 emissions leakage. Emission intensity is understood to mean both direct and indirect emissions from the sector concerned. Indirect emissions, such as those caused by electricity consumption, are determined by means of an electricity emission factor.

![]()

The respective amount of aid is to be calculated using a benchmark approach, analogous to the European emissions trading system. In order to be eligible for the respective aid, the companies should, as a counterpart, provide evidence that they have introduced an energy management system (EnMS) and are implementing measures to improve energy efficiency and decarbonisation.

While energy-intensive companies (consumption of more than 500 MWh per year) must demonstrate a certified EnMS according to ISO 50.001 or an environmental management system according to EMAS, smaller companies must be able to demonstrate a gradual (until 2023) non-certified EnMS based on ISO 50.005.

Author: Sina Barragan, GALLEHR+PARTNER

GALLEHR+PARTNER® supports affected companies on all issues related to the Fuel Emissions Trading Act (SESTA) and the National Emissions Trading Scheme (nEHS)

We carry out the following activities:

- Determining the impact of the Fuel Emissions Trading Act (SESTA) on your company

- Advice for possible switch to EU-ETS

- Review of client contracts for need of amendment with regard to SESTA

- Preparation and submission of the monitoring plan in accordance with §6 BEHG and continuous monitoring up to approval

- Verifiable determination of fuel emissions and preparation of the emissions report pursuant to § 7 para. 1, 2 SESTA

- Preparation and support of the verification of the emission report according to § 7 para. 3 SESTA

- Transmission of the verified emissions report to the competent authority (DEHSt) by 31.07 of the following year in accordance with §7 Para. 1 SESTA

- Verification of the avoidance of double charging in accordance with §7 Para. 5 SESTA

- Support in the establishment of accounts and account representatives in the national emissions trading registry pursuant to section 12 para. 2 SESTA for the administration of emission allowances pursuant to section 9 para. 1

- Support in the management of their register account e.g. as one of the authorized account holders

- Verification of transfers

- timely retransfers of emission allowances by 30.09 for the previous year pursuant to § 8 SESTA

- Data updates of information in the register

- Representation of historical account movements and balances on the basis of account statements

- Support in the purchase and sale of emission certificates

- Support with requests for information and assistance with on-site inspections by the competent authority pursuant to § 14 SESTA

- Identification of emission allowance price drivers and market monitoring

- Ad hoc announcements on relevant events, political developments and legislative changes

- Regular status and strategy meetings to strengthen decision-making capacity